One of the most persistent concerns among people approaching retirement is straightforward but not simple to answer: How do I make my money last? With longer life expectancies, market unpredictability, persistent inflation, and rising healthcare costs, converting a lifetime of savings into reliable retirement income is one of the most complex financial challenges families face today.

The bucket strategy for retirement is a widely recognized income planning framework that financial professionals use to help organize retirement assets around time and purpose. Rather than treating your portfolio as one undifferentiated pool of money, the bucket approach divides assets into distinct segments — each tied to a specific time horizon and role in your overall income plan.

This article explains what the retirement bucket strategy is, how each bucket functions, what it is designed to address, and what limitations to keep in mind when evaluating whether this framework may be appropriate for your situation. If you are already working through your broader plan, our Retirement & Income Planning page explores many of the interconnected decisions that surround this conversation.

What Is the Bucket Strategy for Retirement?

The bucket strategy for retirement — sometimes called the time-segmentation strategy — is a retirement income planning framework that organizes your savings and investments based on when you expect to need them. Instead of managing a single pool of assets and drawing from it uniformly, the strategy separates retirement assets into multiple “buckets,” each designed to serve a different purpose over a different time frame.

The concept is often credited to financial planner Harold Evensky, who popularized the idea of separating short-term spending needs from longer-term, growth-oriented assets. While implementations vary by individual circumstances and advisor approach, most versions use a three-bucket model. Each bucket carries a different risk profile and is intended to be drawn from at a different point in retirement.

It is important to understand that the bucket strategy is a planning framework, not an investment product. It does not guarantee income, eliminate investment risk, or predict market outcomes. It is a way of organizing and thinking about retirement assets that may help align your portfolio’s structure with your income needs and risk tolerance over time — and it works best as one component of a broader, coordinated retirement investment plan.

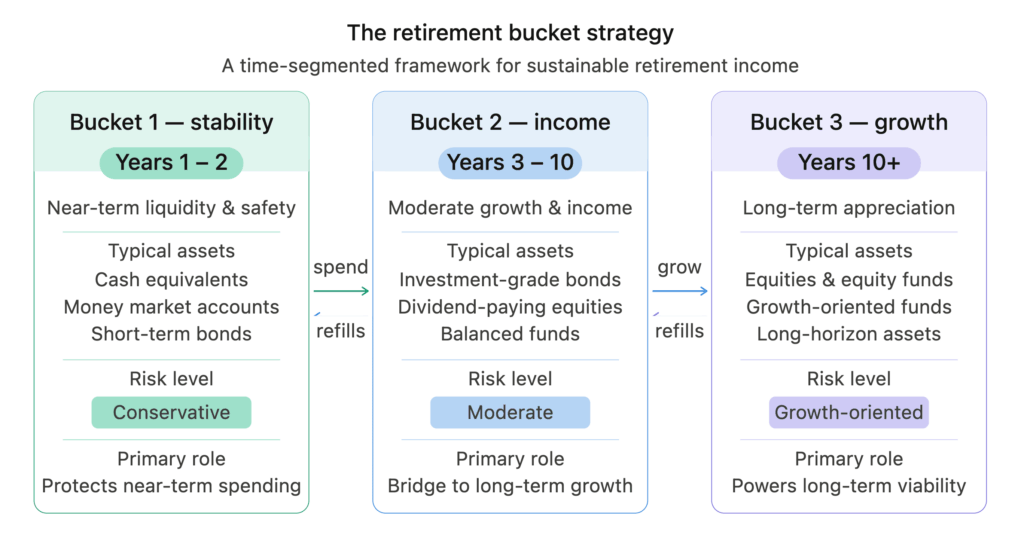

How the Three Buckets Work

Bucket One: Short-Term Stability (Years 1–2)

The first bucket holds assets needed to cover living expenses in the near term — typically the first one to two years of retirement. Because these funds must be stable and readily accessible, they are generally held in cash, money market accounts, or short-term, high-quality fixed income instruments. The objective of Bucket One is not growth — it is stability and liquidity.

The practical benefit of this bucket is that it is designed to insulate retirees from being forced to sell longer-term investments at an inopportune time — such as during a market decline. This is often described as managing sequence-of-returns risk: the risk that poor investment returns early in retirement, when withdrawals begin, could permanently impair your portfolio’s longevity. With Bucket One in place, a retiree can continue drawing income even if markets are experiencing a significant downturn, giving Buckets Two and Three time to potentially recover. This directly connects to how we think about withdrawal strategy planning for our clients.

Bucket Two: Medium-Term Income (Years 3–10)

The second bucket bridges the gap between Bucket One’s short-term stability and Bucket Three’s long-term growth potential. Assets in this bucket typically carry moderate risk and may include investment-grade bonds, dividend-paying equities, balanced funds, or similar income-generating investments. The specific composition will vary based on individual goals, risk tolerance, and overall financial plan — this is where asset allocation decisions become particularly meaningful.

Bucket Two is designed to be drawn from over a three-to-ten-year horizon, with assets periodically moved into Bucket One to replenish it as funds are spent. The moderate risk profile means this bucket has the potential for some growth while remaining more conservative than the long-term growth bucket.

Bucket Three: Long-Term Growth (Years 10+)

The third bucket carries the longest time horizon and is typically invested in more growth-oriented assets, which may include equities or other investments with higher potential returns — and correspondingly higher risk. Because this money is not expected to be needed for a decade or more, it is designed to remain invested long enough to potentially weather market cycles without requiring a near-term sale.

Over time, realized gains or appreciation from Bucket Three may be used to replenish Bucket Two, continuing the cycle. This is where long-term portfolio growth is primarily intended to occur. As with all investing, there is no guarantee of returns, and loss of principal is possible. The thoughtful construction of this bucket is one of the most consequential long-term decisions in the strategy.

Why Retirees and Pre-Retirees Consider the Bucket Strategy

The retirement bucket strategy addresses several behavioral and structural challenges that retirees commonly face:

Emotional clarity during market volatility. When markets decline, retirees drawing from a single portfolio can feel compelled to reduce spending, sell investments at a loss, or make reactive decisions. Knowing that near-term expenses are already covered by Bucket One may reduce anxiety and support more disciplined, long-term decision-making during downturns.

Alignment between risk and time horizon. Not all retirement assets need to carry the same risk profile. Money needed next year should behave very differently than money not needed for fifteen years. The bucket strategy makes this alignment explicit and visible — which is one reason many clients find it easier to stay the course during periods of volatility.

A structured framework for withdrawal planning. Rather than withdrawing arbitrarily from whatever account is most convenient, the bucket approach encourages intentional withdrawal sequencing. This connects directly to broader tax-aware distribution planning — including how and when to draw from taxable accounts, tax-deferred accounts, and Roth accounts. For a deeper look at this, visit our page on Withdrawal Strategies.

Potential Benefits Worth Understanding

The bucket strategy offers several potential benefits that may make it worth considering as part of your retirement income plan:

- Liquidity planning: Bucket One ensures accessible funds for near-term needs without requiring the liquidation of long-term assets at an unfavorable time.

- Behavioral support: A clear, organized structure may reduce reactive decision-making during periods of market volatility — one of the most common and costly mistakes in retirement.

- Time horizon alignment: Each bucket’s risk level is explicitly matched to how soon those assets may be needed, supporting a more intentional approach to investment time horizon planning.

- Flexibility over time: The framework can be adapted as income needs, tax situations, health circumstances, or broader financial priorities evolve throughout retirement.

These potential benefits do not eliminate investment risk and will not be experienced identically by every retiree. Individual outcomes depend on many factors, including portfolio size, spending rate, market conditions, and how consistently the strategy is implemented and reviewed.

Limitations and Considerations to Keep in Mind

No retirement income strategy is without trade-offs. Understanding the limitations of the bucket strategy is just as important as understanding its benefits:

Refilling decisions can be subjective. Deciding when and how to move assets from one bucket to another involves judgment calls that may not always be straightforward, particularly during prolonged market downturns when Bucket Three has declined in value.

Increased complexity. Managing three distinct segments of a portfolio requires more ongoing oversight, coordination, and review than a single unified portfolio approach.

Tax implications. Selling appreciated assets in Bucket Three to refill Bucket Two can trigger taxable events. This makes tax-aware planning a critical element of how the strategy is managed over time. Oxford Investment Group does not provide tax or legal advice; clients should consult a qualified tax professional for guidance specific to their situation.

Not a standalone solution. The bucket strategy works best when integrated into a comprehensive retirement income plan that also addresses Social Security timing, Required Minimum Distributions (RMDs), healthcare expenses, legacy planning, and ongoing income reviews.

How the Buckets Are Typically Refilled Over Time

A common question about the bucket strategy is: how does Bucket One get replenished once it begins to be spent down? While there is no universal rule — and the right approach depends on individual circumstances — refilling often involves one or more of the following:

- Transferring income generated by Bucket Two (dividends, bond interest) into Bucket One on a regular basis.

- Rebalancing Bucket Three during periods of market appreciation and moving a portion of gains into Bucket Two, which in turn is used to refill Bucket One.

- Directing other income sources — such as Social Security benefits, pension payments, or Required Minimum Distributions — toward near-term expenses, reducing how often assets need to be drawn from Bucket One.

The refilling process should be reviewed regularly as part of ongoing investment management, and adjusted as market conditions, income needs, tax situations, or life circumstances change.

Is the Bucket Strategy for Retirement Right for You?

The bucket strategy can be a useful framework for many retirees and pre-retirees — particularly those who want a clear, organized structure for thinking about retirement income and who benefit from knowing that near-term expenses are insulated from market volatility. However, whether it is appropriate for your specific situation depends on a number of individual factors, including:

- Your total retirement assets relative to expected spending needs

- Your available income sources, including Social Security, pensions, or part-time income

- Your investment time horizon and personal comfort with risk

- Your tax situation and the types of accounts you hold

- Your broader retirement goals and priorities, including legacy and healthcare planning

The bucket strategy is not a one-size-fits-all answer. It is one framework among several — alongside systematic withdrawal strategies, floor-and-upside approaches, and income annuity structures — that may be evaluated as part of a personalized, fiduciary-guided retirement income plan.

Working with a fiduciary financial advisor allows you to evaluate these options in the context of your full financial picture — not just the strategy itself, but how it interacts with your taxes, your estate plan, your insurance coverage, and your income sources over a retirement that may span two to three decades or more.

Frequently Asked Questions About the Bucket Strategy for Retirement

What is the bucket strategy for retirement in simple terms?

The bucket strategy is a retirement income planning framework that divides your savings and investments into separate segments — called buckets — based on when you expect to need the money. A short-term bucket holds stable, accessible funds for near-term expenses. A medium-term bucket holds moderate-risk assets intended to be drawn on over several years. A long-term bucket holds growth-oriented investments not expected to be needed for a decade or more. Together, the three buckets are designed to provide near-term stability while maintaining long-term growth potential.

How many buckets should a retirement portfolio have?

Most implementations of the bucket strategy use three buckets organized around short-, medium-, and long-term time horizons. Some advisors use two buckets or four, depending on an individual’s income needs, portfolio complexity, and planning preferences. The number of buckets matters less than ensuring each segment serves a clearly defined purpose and is aligned with your overall time horizon and risk tolerance within a broader financial plan.

What types of investments are typically placed in each bucket?

This varies based on individual circumstances, risk tolerance, and the overall financial plan. Generally speaking, Bucket One may hold cash or cash equivalents such as money market accounts; Bucket Two may hold moderate-risk income-generating assets such as bonds or dividend-paying equities; and Bucket Three may hold growth-oriented assets such as stocks or equity funds. Specific investment selections should always be made in the context of a personalized plan developed with a qualified financial advisor. All investing involves risk, including the possible loss of principal.

How does the bucket strategy help address sequence-of-returns risk?

Sequence-of-returns risk is the danger that poor market performance early in retirement — when withdrawals have already begun — can permanently damage a portfolio’s longevity, even if long-term returns eventually recover. The bucket strategy attempts to address this by keeping near-term expenses in stable, accessible assets, reducing the need to sell growth-oriented investments during a market decline. This does not eliminate investment risk or guarantee a specific outcome, but it may help retirees avoid locking in losses during periods of market volatility by providing an alternative source of near-term income.

How is the bucket strategy different from the 4% withdrawal rule?

The 4% rule is a withdrawal rate guideline suggesting that withdrawing approximately 4% of your initial portfolio annually, adjusted for inflation, has historically supported a 30-year retirement in many scenarios. The bucket strategy is a structural framework for organizing and managing retirement assets — it is not a withdrawal rate formula. The two are not mutually exclusive; many advisors integrate withdrawal rate guidelines into a bucket framework as part of a broader withdrawal strategy. The 4% rule is a general guideline, not a guarantee; actual outcomes depend on market conditions, individual spending patterns, inflation, and portfolio composition.

When should I start implementing a bucket strategy?

Many financial professionals suggest beginning to structure a bucket approach five to ten years before retirement — a period sometimes called the “transition zone.” This window allows time to gradually shift asset allocation toward the intended bucket structure, build Bucket One reserves, and coordinate the strategy with Social Security timing, tax planning, and other income sources. That said, the bucket framework can also be relevant for individuals who are already in retirement and want more structure and clarity around income and withdrawals going forward.

Does the bucket strategy guarantee I won’t run out of money in retirement?

No. No retirement income strategy eliminates the risk of outliving your assets. The bucket strategy is designed to provide structure, behavioral discipline, and time-horizon alignment — but it does not guarantee specific outcomes. Its long-term effectiveness depends on factors including portfolio size, spending rate, market performance, inflation, longevity, and how consistently the strategy is reviewed and maintained over time. Working with a fiduciary financial advisor can help you evaluate income sustainability as part of a comprehensive retirement plan that accounts for these uncertainties.

Can the bucket strategy be combined with Social Security and other income sources?

Yes — and in most cases, it should be. The bucket strategy works alongside, and often depends on, other retirement income sources. Social Security benefits, pension payments, Required Minimum Distributions (RMDs), rental income, or part-time employment can all influence how each bucket is structured, how much needs to be held in Bucket One, and how frequently assets need to move between buckets. A fully coordinated plan that accounts for all income sources and their timing is generally more effective than managing any single strategy in isolation.

Explore Your Retirement Income Options With Oxford Investment Group

Oxford Investment Group is a fiduciary financial services firm headquartered in Raleigh, North Carolina, with more than 40 years of experience serving individuals, families, and business owners. Our team works with clients across the Triangle and throughout North Carolina to evaluate retirement income frameworks — including the bucket strategy — within the context of a comprehensive, personalized financial plan.

We do not sell products or operate on commission. As fiduciaries, we are obligated to act in your best interest — and that means helping you understand your options, the trade-offs involved, and how different strategies fit your specific situation, not pushing a one-size-fits-all solution.

If you are approaching retirement or already in it and want to explore how to structure your assets for income, sustainability, and long-term clarity, we invite you to start with a conversation.

→ Explore Retirement & Income Planning

→ Learn About Our Investment Management Services

→ Work With a Fiduciary Financial Advisor

Disclosure: This article is intended for educational and informational purposes only. It does not constitute personalized investment, tax, or legal advice, and should not be relied upon as a recommendation to buy or sell any specific security or to adopt any particular investment or withdrawal strategy. All investing involves risk, including the possible loss of principal. Past performance does not guarantee future results. Individual outcomes will vary based on personal financial circumstances, market conditions, portfolio composition, spending patterns, and other factors that are beyond the control of Oxford Investment Group, Inc. The bucket strategy is a general planning framework; its suitability for any particular individual depends on that individual’s specific financial situation, goals, and risk tolerance. Oxford Investment Group, Inc. does not provide tax or legal advice. Clients and prospective clients should consult qualified tax and legal professionals regarding their individual situations before implementing any financial strategy. Oxford Investment Group, Inc. is a Registered Investment Adviser. Registration does not imply a certain level of skill or training. For more information, please visit our website or contact our office directly.