Social Security vs. Pension Income Strategies

As retirement approaches, one of the most critical questions couples face isn’t “Do we have enough saved?”—it’s “How do we turn what we’ve saved into reliable income?”

Social Security and pension income serve different roles in retirement. Social Security may provide inflation-adjusted lifetime income, while pensions may provide predictable employer-sponsored income with different payout and survivor options. The right strategy depends on claiming age, tax considerations, pension elections, survivor needs, and how these sources coordinate with savings and investment accounts.

Financial Empowerment for Women Over 50

Entering your 50s often brings a sharper focus on what matters most: independence, flexibility, health, family, and how your money will support the next stage of life. For many women, this decade becomes a financial turning point. Retirement is closer, caregiving responsibilities may shift, and major life changes such as divorce, widowhood, career transitions, or helping aging parents can create new planning needs. Financial empowerment for women over 50 is not about chasing complicated strategies or trying to predict the markets. It starts with clarity. When you understand your income sources, savings, investments, risks, and choices, you can make more informed decisions about retirement, taxes, insurance, estate planning, and long-term security.

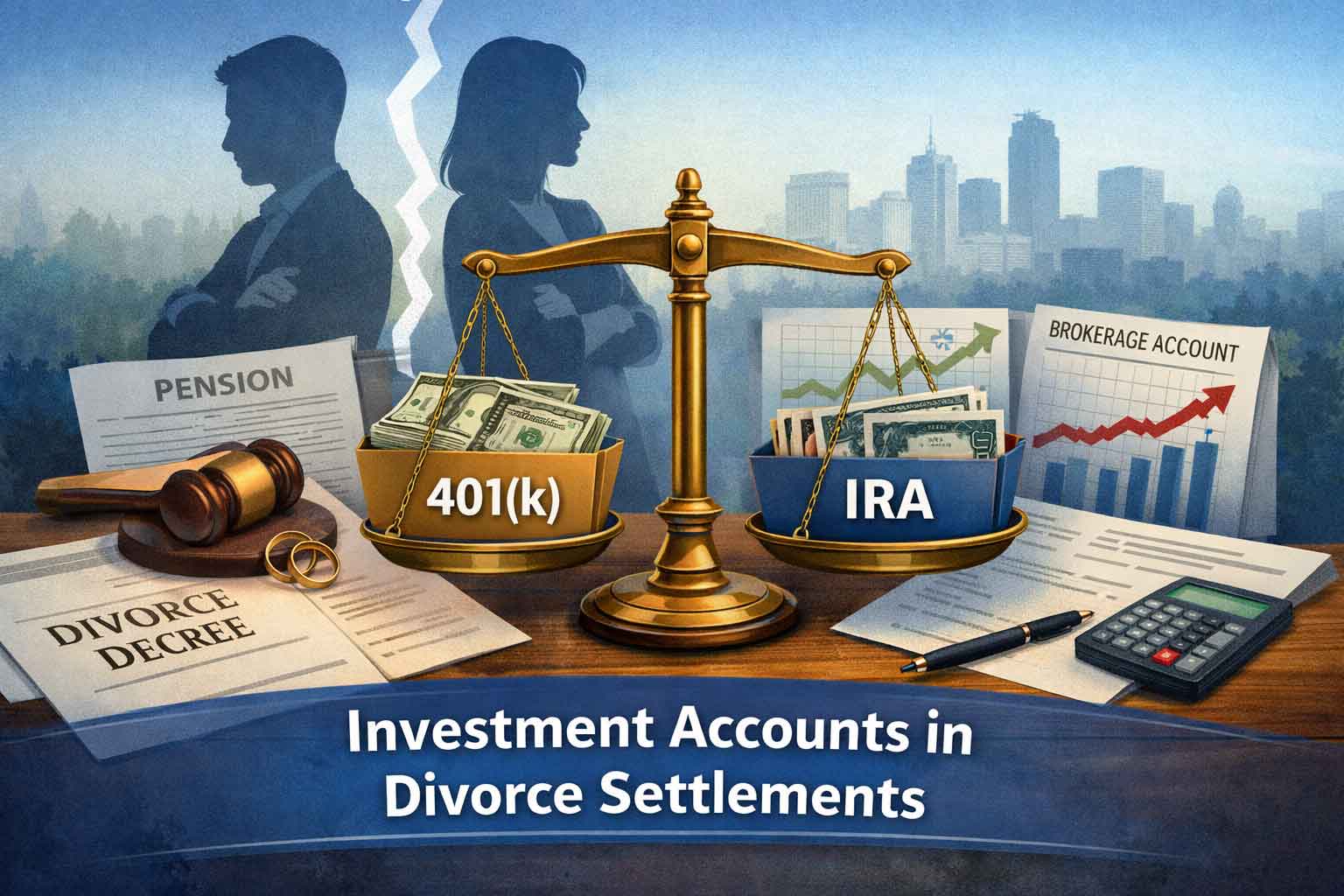

Investment Accounts in Divorce Settlements: What to Know

Divorce can create major financial change, and one of the most important issues to understand is how investment accounts in divorce settlements are handled. Retirement plans, IRAs, brokerage accounts, pensions, and stock compensation may all be part of the discussion, but they do not all work the same way. Differences in tax treatment, liquidity, withdrawal rules, and plan administration can materially affect long-term outcomes. IRS guidance confirms that transfers because of divorce are often handled under special tax rules, and retirement-plan divisions may require specific court orders or plan-approved documentation depending on the account involved.

How to Know When You’re Ready to Retire

Retirement is not just a number on a calendar. For most people, it is a financial transition, a lifestyle transition, and an emotional transition all at once.

If you are wondering how to know when you’re ready to retire, the answer usually comes down to whether your income sources, spending needs, health coverage, tax picture, and long-term goals are aligned well enough to support the life you want. It is less about finding a single “magic number” and more about determining whether your plan appears sustainable under a range of real-world conditions.

The Ultimate Estate Planning Checklist for North Carolina Families

Estate planning checklist: the fast way to protect your family, name decision-makers, and keep your plan organized. If you’re a North Carolina parent, homeowner, business owner, or simply someone with people who depend on you, an estate plan helps answer two questions:

Who’s in charge if you can’t make decisions?

Who gets what—and how—when you’re gone?

This guide breaks estate planning into clear, practical steps you can complete with the right professionals.

Understanding Required Minimum Distributions (RMDs): Rules, Ages, and Planning Considerations

Required Minimum Distributions (RMDs) are one of the most important rules governing retirement accounts. While tax-advantaged accounts such as traditional IRAs and 401(k)s allow investments to grow tax-deferred, the IRS eventually requires withdrawals so those funds can be taxed. Understanding Required Minimum Distributions (RMDs) can help retirees avoid penalties, plan retirement income more effectively, and coordinate withdrawals with taxes, Social Security, and other financial priorities.

Why Working with a Fiduciary Financial Advisor May Be Worth Considering

You’re sitting across from a financial professional, reviewing a proposal for your retirement portfolio. The plan seems sound, the investments familiar. But a quiet question lingers in the back of your mind: Is this truly the best possible advice for me, or just the most profitable recommendation for them?

This single, often unspoken, question is the most critical one in your financial life. The answer separates a standard client-advisor relationship from a true partnership. It’s the difference between advice that is merely “appropriate” and advice that is legally and ethically bound to your best interest.

Proactive Tax Planning Strategies to Lower Your Bill in North Carolina (2025 Guide)

High-income professionals, business owners, retirees, and families in NC benefit most when tax planning is coordinated year-round and integrated with retirement, investment, and estate strategies. This guide explains how tax planning works, what strategies are available in 2025, and how North Carolina tax rules affect your plan.

How to Choose the Right Financial Advisor for Your Situation

Major life changes—such as retirement, divorce, receiving an inheritance, selling a business, or navigating a career transition—often bring with them a mix of opportunity and uncertainty. These moments can reshape your financial landscape in ways that are both deeply personal and financially significant. While some individuals may feel comfortable managing certain aspects of their finances on their own, many reach a point where professional guidance becomes essential for making informed, well-structured decisions.

Tax-Smart Ways to Transfer Business Ownership

Transferring ownership of a business is more than a financial transaction—it’s a decision that affects employees, customers, family members, and future legacy. The way the transition is structured can significantly influence how much of the proceeds an owner keeps after taxes. Planning ahead, understanding available strategies, and coordinating advisors can help support a smoother, more intentional transition process.